Why India’s Medical-Devices Market Is Broken

India’s medical-devices sector especially for advanced diagnostics and therapeutic equipment is beset by structural challenges that suppress local innovation, concentrate capabilities in a few metros, and keep prices unaffordable for the vast middle class. Yet these very pain-points create clear investment “greenfields” for funds willing to back novel financing models, regulatory-savvy startups, and integrated service platforms.

1. Market Overview & Pain Points

Low domestic manufacturing & scale: 90 % of CT/MRI/PET-CT/digital X-ray units are imported (Siemens, GE, Philips).

High capex & op-ex: ₹10–15 crore per MRI; AMCs at 10–15 % of capex annually.

Regulatory drag: 12–18 month approval cycles under CDSCO’s phased Medical Device Rules (2017–22).

Fragmented procurement: Hospitals negotiate individually, public tenders prize lowest cost over lifecycle value.

2. Key Barriers & Investment Themes

Upfront Capital Expenditure Requirements

Barrier: Hospitals and diagnostic centers must pay ₹5–15 crore per advanced device (MRI, CT, digital X-ray) before they start generating any revenue from it.

What’s Driving It:

High manufacturing and import costs for precision hardware.

Banks view standalone medical devices as illiquid collateral, so financing is scarce or expensive.

Smaller facilities lack balance-sheet depth to amortize such large investments.

Regulatory Delays & Complexity

Barrier: Getting a new device approved under India’s Medical Device Rules often takes 12–18 months of submissions, clinical trials, and multiple agency sign-offs.

What’s Driving It:

Overlapping jurisdictions (CDSCO, BIS, state FDAs) each impose distinct documentation, testing, and quality-system requirements.

Regulators prioritize safety and imported-device scrutiny, creating lengthy review cycles.

Domestic innovators lack in-house regulatory expertise, multiplying back-and-forth with authorities.

Skilled Personnel Shortage

Barrier: There are fewer than one trained biomedical engineer or radiography technician per 100 hospital beds, leading to under-utilization and errors.

What’s Driving It:

Limited number of accredited training institutes; existing curricula lag behind modern device complexity.

High attrition in tier-2/3 locations as technicians migrate to metros or non-clinical roles.

Hospitals do not invest sufficiently in ongoing up-skilling or certification pathways.

Opaque Pricing & Billing Practices

Barrier: No standardized price lists for device-driven procedures—each hospital applies its own markups—so patients and insurers cannot predict costs.

What’s Driving It:

Lack of regulatory price controls except for a short “essential devices” list.

Hospitals view device usage as a profit center and dynamically adjust rates based on demand and case complexity.

Insurers push back on high claims, leading to negotiation-driven billing rather than transparent pricing.

Low Local R&D & “Made-for-India” Innovation

Barrier: India produces almost no homegrown advanced diagnostic devices; >90 % of high-end units are imported.

What’s Driving It:

R&D spend in India is below 0.1 % of GDP, with scant venture capital for hardware startups.

Weak collaboration between engineering institutes, hospitals, and industry to co-develop prototypes.

Multinational companies focus on larger, high-margin markets, leaving cost-sensitive segments unaddressed.

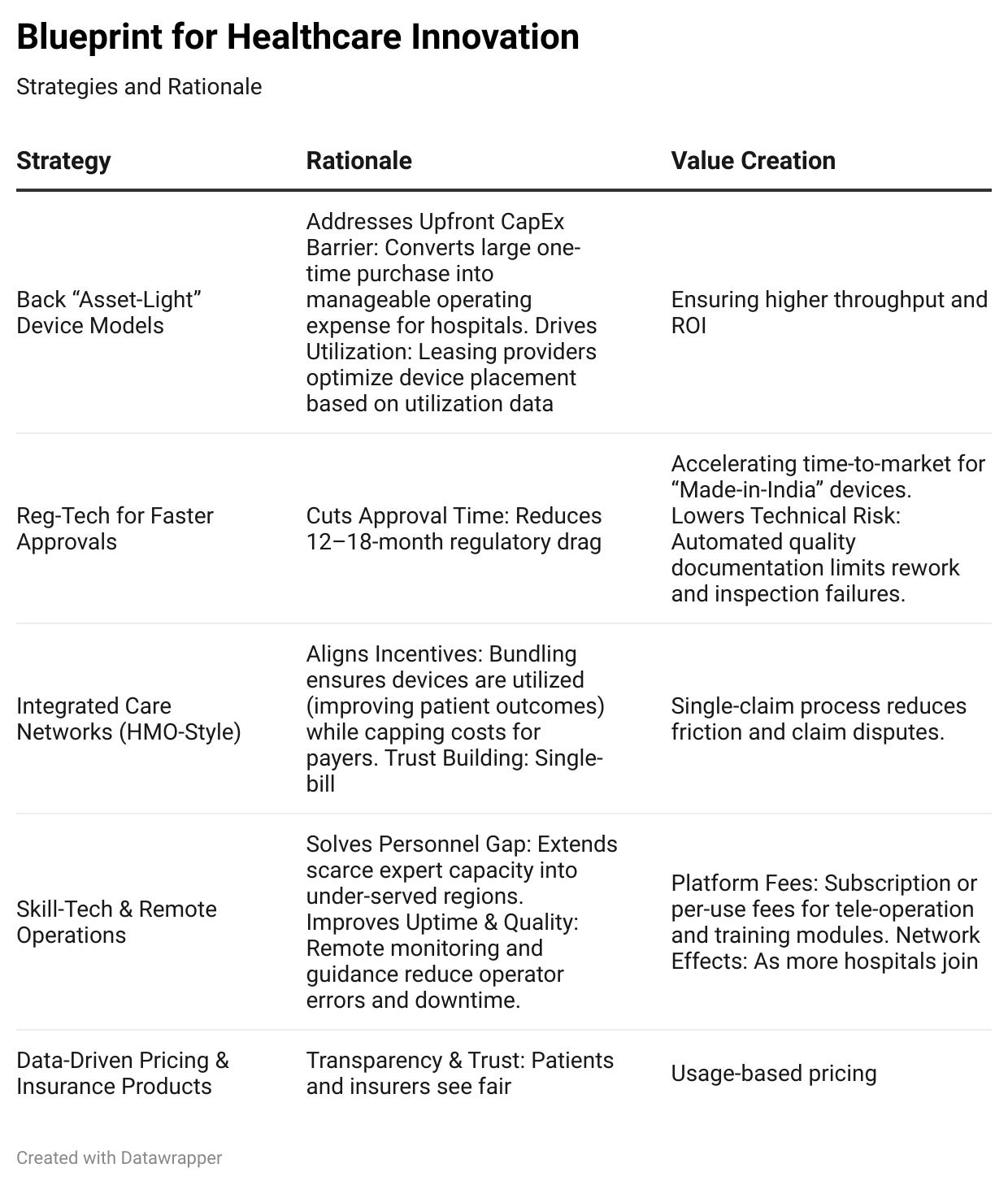

3. Strategic Recommendations

4. Emerging Innovators

Indian entrepreneurs are tackling every segment of devices with ingenuity:

Diagnostics: Homegrown innovators are delivering fast, AI-powered tests. For example, Bengaluru’s Tricog Health has pioneered 24×7 AI–powered ECG analysis: its InstaECG service (cloud–based ECG diagnosis) is used in 5,000+ hospitals and clinics, screening over 10 million patients worldwide and saving thousands of lives. Niramai Health uses AI-enabled thermal imaging to screen for breast cancer and other conditions non-invasively, addressing early-detection gaps in women’s health. These AI-driven diagnostics from portable blood analyzers to smart X-ray units promise lab-quality results in village clinics and urban community centers alike.

Therapeutic devices (e.g. ophthalmic devices): In eye care, Forus Health (Bengaluru) has made waves with 3Nethra – a portable, AI-assisted retinal camera. Forus’s founder designed 3Nethra to screen for diabetic retinopathy and other blindness-causing diseases in minutes. Today 3Nethra devices have screened over 2 million patients in India and 20+ other countries, often administered by minimally trained staff at rural camps. By automating diagnosis, Forus brings timely treatment (like laser therapy) within reach, exemplifying affordable therapeutic innovation.

Surgical robotics: SS Innovations (Gurugram/Noida) is commercializing SSI Mantra, India’s first indigenously built surgical robots. SSI Mantra features five robotic arms, a 3D-HD surgeon console and advanced instrument control. Doctors at Pune’s Noble Hospital report it enables highly precise, minimally invasive surgery (smaller incisions, faster recoveryIts founder envisions that telesurgery with SSI Mantra will “decentralize and democratize surgical expertise” – bringing complex cardiovascular and neuro surgeries to smaller centers.

Health monitoring & wearables: Wearables and home devices are saving lives via continuous monitoring. Dozee offers a contactless bedside sensor that uses ballistocardiography to track heart rate, respiration and sleep –alerting clinicians to emergencies hours before symptoms appear. Dozee’s FDA-cleared system is already used in 300+ hospitals monitoring over 1 million patients each year. HealthCube builds portable diagnostic analyzers: a laptop-sized unit that can perform dozens of blood tests (anemia, malaria, diabetes, etc.) on battery power. This empowers frontline health workers in remote areas to run lab-grade tests without electricity.

Together, these innovators illustrate India’s device renaissance homegrown solutions adapted to local needs. They also offer replicable models for global markets facing similar challenges.

The medtech market’s rapid growth and fragmentation spell high returns for early backers. With India now among the world’s top 20 markets (and growing from $12B to ~$50B by 2030 according to EY and global giants eyeing India as an innovation hub, there’s deep demand to be tapped.

Hospitals and clinics: New business models and devices lower the cost of care. Leasing and pay-per-use schemes mean even smaller hospitals can install advanced scanners and surgical tools. Integrated platforms (devices + software) streamline operations: for example, robotic-assisted surgery significantly cuts complication rates and shortens patient stays. AI triage and teleradiology reduce overload on specialists, letting a single expert serve many more patients remotely. In short, providers improve throughput and quality: they can treat more patients with better outcomes, without proportionally higher costs.

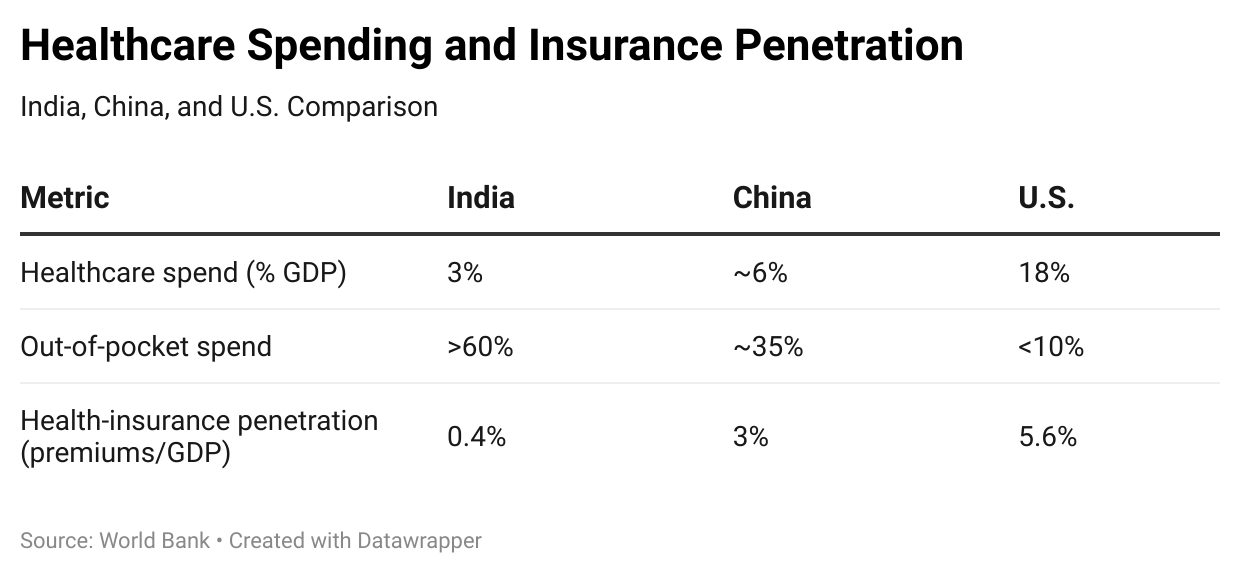

Insurers and payers: Advanced devices and analytics mean more predictable costs. Continuous monitoring and early diagnostics catch complications early, reducing expensive ICU stays. Data from wearables and clinics feed into smarter underwriting: Peak XV-backed plans like Kenko’s micro-insurance use granular health data to price ultra-affordable plans (covering meds, doctors and diagnostics for under ₹200/month. As insurance penetration rises from today’s 37% towards universal coverage, tech-driven insurers can control claims more precisely and extend coverage to low-income groups. In effect, devices become tools for population health management – saving insurers money over the long run.

Patients: Ultimately, people win. Affordable point-of-care diagnostics and wearables mean earlier detection of diabetes, heart disease or cancer – often before symptoms strike. Patients in small towns will no longer have to travel to big cities for basic tests or scans. Chronic disease management (via remote monitors and tele-doctors) keeps people healthier at home. And financial protection improves: integrated care networks and “health-as-a-service” plans mean patients pay predictably (and often less overall), avoiding catastrophic bills.

I see a future where “affordable excellence” is not an oxymoron but the norm: where every hospital has the tools to diagnose and treat effectively, and every patient has access to world-class care.